Blockchain for Identity and Lending

Table of Contents

1. Overview

This research explores the intersection of blockchain technology with digital identity systems and decentralized lending protocols. Traditional lending relies on centralized credit bureaus and identity verification systems that exclude billions of people from financial services. Blockchain-based identity (self-sovereign identity) combined with decentralized finance (DeFi) lending protocols offers potential for more inclusive credit systems while maintaining necessary KYC/AML compliance.

2. Background

2.1. Traditional Identity and Credit Systems

Centralized credit bureaus (Equifax, Experian, TransUnion in the US) maintain credit histories used by lenders to assess risk. These systems face several challenges:

- Data breaches: 2017 Equifax breach exposed 147 million records

- Limited coverage: Credit-invisible populations cannot access loans

- Geographic fragmentation: Credit history does not travel across borders

- Single points of failure: Centralized databases create systemic risk

- Privacy concerns: Individuals have limited control over their data

2.2. The Unbanked Problem

World Bank estimates 1.4 billion adults remain unbanked globally. Many more are "credit invisible"—lacking sufficient credit history to qualify for traditional loans. This excludes them from:

- Mortgage lending

- Small business financing

- Consumer credit

- Insurance products

2.3. Blockchain as Trust Infrastructure

Blockchain enables new approaches to identity and lending:

- Immutable credential storage

- User-controlled data sharing

- Transparent lending protocols

- Collateralized lending without credit checks

- Reputation systems based on on-chain activity

3. Key Concepts

3.1. Self-Sovereign Identity (SSI)

SSI places individuals in control of their digital identity. Key components:

- Decentralized Identifiers (DIDs): W3C standard for verifiable identifiers

- Verifiable Credentials (VCs): Cryptographically signed attestations

- Identity wallets: User-controlled storage for credentials

- Zero-knowledge proofs: Prove attributes without revealing underlying data

Example: Prove you are over 18 without revealing your birthdate or full ID.

3.2. DeFi Lending Protocols

Decentralized lending protocols enable peer-to-pool lending without intermediaries:

3.2.1. Over-Collateralized Lending

- Aave: Flash loans, variable/stable rates, multi-chain

- Compound: Algorithmic interest rates, cToken model

- MakerDAO: DAI stablecoin minting against collateral

These protocols require collateral exceeding loan value (typically 150%+), limiting their utility for credit-constrained borrowers.

3.2.2. Under-Collateralized and Identity-Based Lending

- Goldfinch: Real-world asset lending with trust scoring

- TrueFi: Unsecured lending to verified borrowers

- Maple Finance: Institutional lending pools

- Centrifuge: Real-world asset tokenization for lending

3.3. Sybil Resistance and Reputation

On-chain identity requires preventing Sybil attacks (one person creating multiple fake identities). Approaches include:

- Proof of Humanity: Video verification with vouching

- BrightID: Social graph analysis

- Gitcoin Passport: Aggregated identity stamps

- Worldcoin: Biometric (iris) verification

3.4. Credit Scoring On-Chain

Projects building on-chain credit scores:

- Spectral Finance: MACRO score from wallet history

- Cred Protocol: Cross-chain credit assessment

- ARCx: DeFi credit score (Sapphire)

- Masa Finance: Soulbound credit reports

4. Implementation

4.1. Identity Layer Architecture

+-------------------+

| User Identity |

| Wallet |

+-------------------+

|

v

+-------------------+ +-------------------+

| DID Registry |<--->| Credential Issuers|

| (Blockchain) | | (KYC providers, |

| | | governments, |

| | | employers) |

+-------------------+ +-------------------+

|

v

+-------------------+

| Lending Protocol |

| - Verify creds |

| - Assess risk |

| - Issue loan |

+-------------------+

4.2. KYC/AML Integration

Compliant DeFi lending requires identity verification:

- User completes KYC with accredited verifier

- Verifier issues credential to user's wallet

- User presents credential to lending protocol

- Protocol verifies signature without accessing raw KYC data

- Loan proceeds with verified identity but privacy preserved

4.3. Smart Contract Lending Flow

// Simplified identity-verified lending

interface ICredentialVerifier {

function verifyCredential(

address borrower,

bytes calldata credential

) external view returns (bool);

}

contract IdentityLending {

ICredentialVerifier public verifier;

function borrow(

uint256 amount,

bytes calldata kycCredential

) external {

require(

verifier.verifyCredential(msg.sender, kycCredential),

"KYC verification failed"

);

// Proceed with under-collateralized loan

// based on verified identity and on-chain history

}

}

4.4. Risk Considerations

- Smart contract risk: Protocol bugs can lose funds

- Oracle risk: Price feeds can be manipulated

- Regulatory risk: Unclear treatment of DeFi lending

- Default risk: Under-collateralized loans have higher default rates

- Privacy vs compliance: Balancing user privacy with AML requirements

5. References

- W3C DID Specification: https://www.w3.org/TR/did-core/

- W3C Verifiable Credentials: https://www.w3.org/TR/vc-data-model/

- Aave: https://aave.com/

- Compound: https://compound.finance/

- MakerDAO: https://makerdao.com/

- Goldfinch: https://goldfinch.finance/

- Proof of Humanity: https://proofofhumanity.id/

6. Notes

- The 2016 timeframe of this research predates the DeFi summer of 2020 and subsequent explosion of lending protocols.

- Self-sovereign identity standards (DIDs, VCs) have matured significantly since initial research.

- Regulatory frameworks like MiCA (EU) and proposed US legislation are beginning to address DeFi lending compliance requirements.

- The fundamental insight—that blockchain can enable identity-based lending with privacy preservation—remains a active area of development in 2024 and beyond.

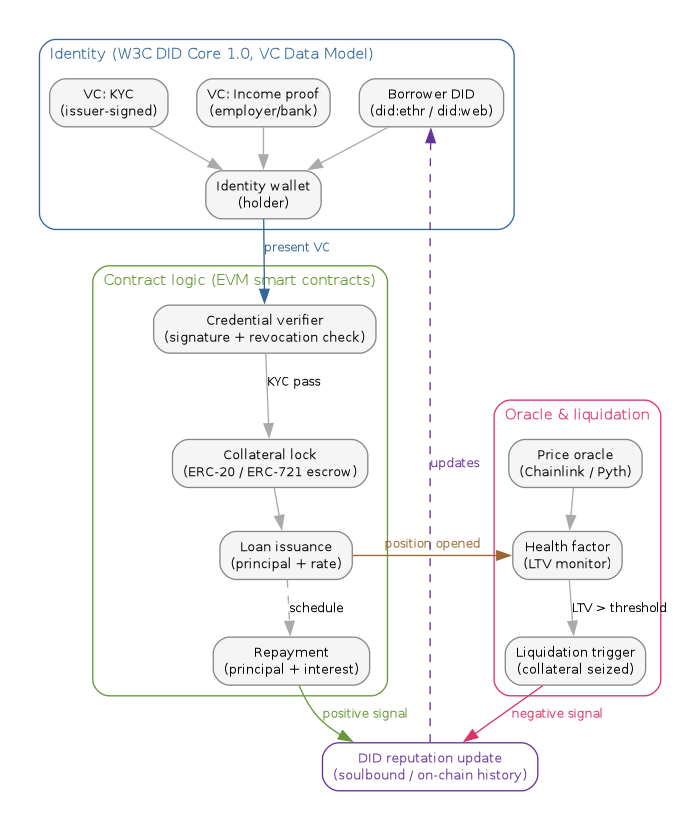

7. Diagram: DID-anchored DeFi lending flow

The flow below shows how a borrower's decentralized identifier (DID) and verifiable credentials feed a smart contract that locks collateral, watches an oracle price feed, and writes outcomes (repayment or liquidation) back to the borrower's reputation. Three clusters: identity, contract logic, oracle/liquidation.

digraph defi_lending_flow { rankdir=TB; graph [bgcolor="white", fontname="Helvetica", fontsize=11, pad="0.3", nodesep="0.3", ranksep="0.45"]; node [shape=box, style="rounded,filled", fontname="Helvetica", fontsize=10, fillcolor="#dbeafe", color="#888"]; edge [color="#888", fontname="Helvetica", fontsize=9, fontcolor="#555"]; // Tailwind 100/700 pastel palette // Identity cluster -- DID + verifiable credentials subgraph cluster_identity { label="Identity (W3C DID Core 1.0, VC Data Model)"; labeljust="l"; color="#1d4ed8"; fontcolor="#1d4ed8"; style="rounded"; borrower_did [label="Borrower DID\n(did:ethr / did:web)", fillcolor="#dbeafe", color="#1d4ed8", fontcolor="#1d4ed8"]; vc_kyc [label="VC: KYC\n(issuer-signed)", fillcolor="#dbeafe", color="#1d4ed8", fontcolor="#1d4ed8"]; vc_income [label="VC: Income proof\n(employer/bank)", fillcolor="#dbeafe", color="#1d4ed8", fontcolor="#1d4ed8"]; wallet [label="Identity wallet\n(holder)", fillcolor="#dbeafe", color="#1d4ed8", fontcolor="#1d4ed8"]; borrower_did -> wallet; vc_kyc -> wallet; vc_income -> wallet; } // Contract logic cluster -- verifier + collateral + loan subgraph cluster_contract { label="Contract logic (EVM smart contracts)"; labeljust="l"; color="#15803d"; fontcolor="#15803d"; style="rounded"; verifier [label="Credential verifier\n(signature + revocation check)", fillcolor="#dcfce7", color="#15803d", fontcolor="#15803d"]; collateral [label="Collateral lock\n(ERC-20 / ERC-721 escrow)", fillcolor="#dcfce7", color="#15803d", fontcolor="#15803d"]; loan [label="Loan issuance\n(principal + rate)", fillcolor="#dcfce7", color="#15803d", fontcolor="#15803d"]; repay [label="Repayment\n(principal + interest)", fillcolor="#dcfce7", color="#15803d", fontcolor="#15803d"]; verifier -> collateral [label="KYC pass"]; collateral -> loan; loan -> repay [style=dashed, label="schedule"]; } // Oracle / liquidation cluster subgraph cluster_oracle { label="Oracle & liquidation"; labeljust="l"; color="#b91c1c"; fontcolor="#b91c1c"; style="rounded"; oracle [label="Price oracle\n(Chainlink / Pyth)", fillcolor="#fee2e2", color="#b91c1c", fontcolor="#b91c1c"]; health [label="Health factor\n(LTV monitor)", fillcolor="#fee2e2", color="#b91c1c", fontcolor="#b91c1c"]; liquidation [label="Liquidation trigger\n(collateral seized)", fillcolor="#fee2e2", color="#b91c1c", fontcolor="#b91c1c"]; oracle -> health; health -> liquidation [label="LTV > threshold"]; } // Reputation update writes back to identity reputation [label="DID reputation update\n(soulbound / on-chain history)", fillcolor="#ede9fe", color="#6b21a8", fontcolor="#6b21a8"]; // Cross-cluster wiring wallet -> verifier [label="present VC", color="#1d4ed8", fontcolor="#1d4ed8"]; loan -> health [label="position opened", color="#a16207", fontcolor="#a16207"]; repay -> reputation [label="positive signal", color="#15803d", fontcolor="#15803d"]; liquidation -> reputation [label="negative signal", color="#b91c1c", fontcolor="#b91c1c"]; reputation -> borrower_did [label="updates", color="#6b21a8", fontcolor="#6b21a8", style=dashed]; }

8. Related notes

- Blockchain border bank – cross-border settlement and the same KYC-credential reuse problem this note describes, but at the correspondent-banking layer rather than the lending-pool layer

- Agent token exchange (2025) – agentic finance presumes the lending and identity primitives sketched here are already on-chain; the agent merely composes them

- Model interpretability and fairness in fintech – on-chain credit scoring inherits every fairness problem of off-chain credit scoring, plus a new one: the model now lives in a smart contract that nobody can patch

- Software design – the verifier/oracle/liquidation split here is a worked example of bounded contexts under adversarial conditions

9. Postscript (2026)

The 2016 framing held up unevenly. DeFi summer (June–September 2020) turned Compound, Aave, and MakerDAO into production lending primitives; total value locked across DeFi crossed USD 10B by September 2020 and peaked near USD 180B in November 2021 (DeFi Llama). Over-collateralization, not identity, did the heavy lifting — credit-invisible borrowers got no relief from these protocols.

The CeFi-meets-DeFi narrative broke in 2022. Terra-UST de-pegged on 9 May 2022 and wiped out roughly USD 40B over the following week. FTX filed for Chapter 11 on 11 November 2022; Sam Bankman-Fried was convicted on seven counts on 2 November 2023 and sentenced to 25 years on 28 March 2024. The collapse made under-collateralized lending pools (Maple, TrueFi, Goldfinch) contract sharply as institutional borrowers — Alameda among them — defaulted.

Identity standards landed during the same window. W3C published DID Core 1.0 as a W3C Recommendation on 19 July 2022 and Verifiable Credentials Data Model 2.0 as a Recommendation on 15 May 2025. The EU's eIDAS 2.0 Regulation (EU) 2024/1183 entered into force on 20 May 2024, mandating that every Member State offer a European Digital Identity Wallet by 2026 and giving verifiable credentials a regulated home.

Agentic finance arrived in April 2026. Coinbase published the x402 specification on 6 May 2025 (HTTP 402 + stablecoin micropayments for machine-to-machine commerce) and the surrounding ecosystem — Skyfire, Nevermined, the Cloudflare Agents Week launch the week of 13 April 2026 — revived bot-native lending UX in a form the 2016 note did not anticipate: the borrower is a software agent whose DID is its operator's, and the loan horizon is seconds.

What did not land: reputation-as-collateral. SourceCred, Spectral's MACRO score, ARCx Sapphire, and Gitcoin Passport all shipped, but no major DAO has issued a meaningfully under-collateralized loan against on-chain reputation alone. Soulbound tokens (Weyl, Ohlhaver, Buterin, May 2022) remain a research direction, not a primitive. The unsolved problem is whoever cracks Sybil resistance without a biometric oracle wins the next cycle.