Blockchain Border Bank Concept

Table of Contents

1. Overview

This research examines the potential for blockchain technology to transform cross-border payments and international remittances. Traditional correspondent banking through SWIFT has dominated international transfers for decades, but faces challenges including high fees (averaging 6-7% for remittances), slow settlement times (2-5 business days), limited transparency, and exclusion of unbanked populations. Blockchain-based alternatives promise near-instant settlement, reduced costs, and greater financial inclusion.

2. Background

2.1. Traditional Cross-Border Payment Infrastructure

The Society for Worldwide Interbank Financial Telecommunication (SWIFT) has served as the backbone of international payments since 1973. The network connects over 11,000 financial institutions across 200+ countries. However, SWIFT itself does not move money—it transmits payment instructions between correspondent banks, each of which adds fees and processing time.

Key limitations of traditional systems:

- Settlement delays: 2-5 business days typical

- High costs: Wire fees plus FX spreads

- Opacity: Senders cannot track payment progress

- Exclusion: Requires traditional banking relationships

- Geopolitical risk: Subject to sanctions and deplatforming

2.2. Blockchain as Settlement Layer

Bitcoin (2009) demonstrated that cryptographically secured distributed ledgers could enable peer-to-peer value transfer without intermediaries. Ripple (2012) specifically targeted cross-border payments with its XRP Ledger. Ethereum (2015) introduced programmable smart contracts enabling more complex financial instruments.

3. Key Concepts

3.1. Stablecoins for Cross-Border Settlement

Stablecoins—cryptocurrencies pegged to fiat currencies—address the volatility problem that makes Bitcoin unsuitable for commercial payments.

Major stablecoins for cross-border use:

- USDC (Circle): Regulated, fully reserved, multi-chain

- USDT (Tether): Largest by market cap, controversial reserves

- DAI (MakerDAO): Decentralized, crypto-collateralized

- PYUSD (PayPal): Traditional fintech entry into stablecoins

3.2. Ripple and XRP

Ripple Labs developed RippleNet specifically for financial institution cross-border payments. The XRP cryptocurrency serves as a bridge currency, enabling conversion between any currency pair without requiring direct liquidity pools.

RippleNet components:

- xCurrent: Messaging and settlement between banks

- On-Demand Liquidity (ODL): Uses XRP for instant settlement

- xVia: API for corporates to send payments

3.3. Central Bank Digital Currencies (CBDCs)

Many central banks are exploring or piloting CBDCs for cross-border payments:

- mBridge: BIS Innovation Hub project with China, UAE, Thailand, Hong Kong

- Project Dunbar: Singapore, Australia, Malaysia, South Africa

- Digital Euro: ECB investigating cross-border retail payments

3.4. SWIFT gpi and Blockchain Integration

SWIFT responded to blockchain competition with SWIFT gpi (global payments innovation), reducing average cross-border payment time from 3-5 days to under 30 minutes for many corridors. SWIFT has also explored blockchain integration through experiments with R3 Corda and Hyperledger.

4. Implementation

4.1. Architecture Considerations

Cross-border blockchain payment systems require:

- Fiat on/off ramps: Converting local currency to/from crypto

- Liquidity management: Ensuring sufficient funds in destination currency

- Compliance infrastructure: KYC/AML for all parties

- FX conversion: Real-time or near-real-time currency exchange

- Settlement finality: Legal certainty that payment is complete

4.2. Technical Stack Example

+------------------+ +-------------------+ +------------------+ | Sender Bank | | Blockchain Layer | | Receiver Bank | | - KYC/AML check |---->| - Smart contracts |---->| - KYC/AML check | | - Fiat to stable | | - Atomic swaps | | - Stable to fiat | | - Compliance | | - Settlement | | - Local payout | +------------------+ +-------------------+ +------------------+

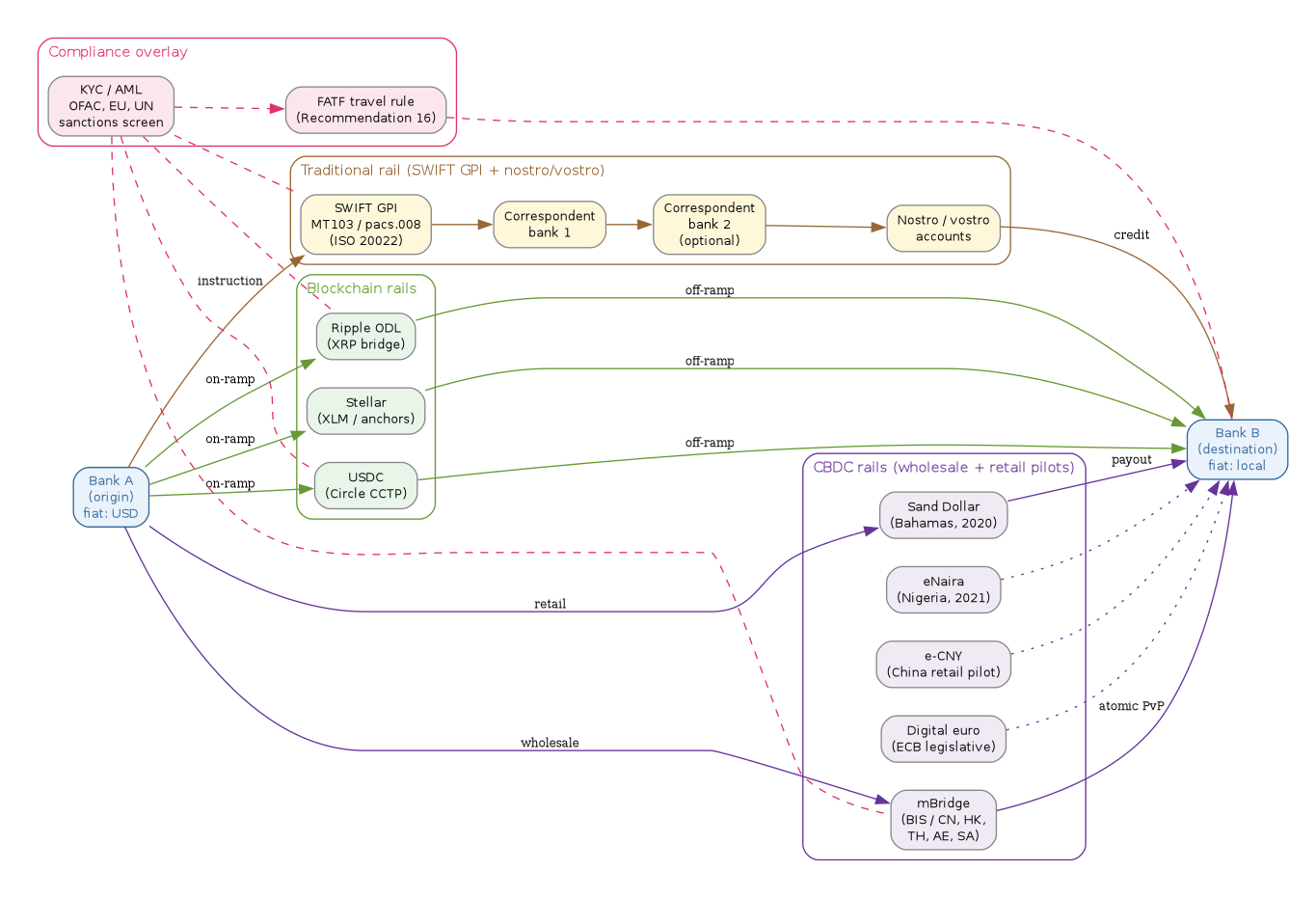

4.3. Settlement-rail comparison diagram

The same Bank-A-to-Bank-B payment can clear through three substantively different rails. The diagram below contrasts the legacy correspondent chain (SWIFT + nostro/vostro accounts), blockchain-native rails (Ripple/XRP, Stellar, USDC), and central-bank rails (mBridge, eNaira, Sand Dollar, e-CNY). KYC/AML and travel-rule overlays apply to all three.

// Cross-border payment settlement -- Bank A (origin) to Bank B // (destination) via three competing rails: traditional SWIFT/Nostro, // blockchain (Ripple/Stellar/USDC), and CBDC (mBridge, Sand Dollar, // eNaira, e-CNY). KYC/AML overlay applies to all rails. digraph cross_border_settlement { rankdir=LR; graph [bgcolor="white", fontname="Helvetica", fontsize=11, pad="0.3", nodesep="0.3", ranksep="0.5"]; node [shape=box, style="rounded,filled", fontname="Helvetica", fontsize=10, fillcolor="#dbeafe", color="#888"]; edge [color="#aaa"]; // Tailwind 100/700 pastel palette // Origin bankA [label="Bank A\n(origin)\nfiat: USD", fillcolor="#dbeafe", color="#1d4ed8", fontcolor="#1d4ed8"]; // Traditional rail: SWIFT messaging + correspondent/nostro chain subgraph cluster_swift { label="Traditional rail (SWIFT GPI + nostro/vostro)"; labeljust="l"; color="#a16207"; fontcolor="#a16207"; style="rounded"; swift_msg [label="SWIFT GPI\nMT103 / pacs.008\n(ISO 20022)", fillcolor="#fef9c3", color="#a16207", fontcolor="#a16207"]; corr1 [label="Correspondent\nbank 1", fillcolor="#fef9c3", color="#a16207", fontcolor="#a16207"]; corr2 [label="Correspondent\nbank 2\n(optional)", fillcolor="#fef9c3", color="#a16207", fontcolor="#a16207"]; nostro [label="Nostro / vostro\naccounts", fillcolor="#fef9c3", color="#a16207", fontcolor="#a16207"]; swift_msg -> corr1 -> corr2 -> nostro [color="#a16207"]; } // Blockchain rail: Ripple, Stellar, USDC bridges subgraph cluster_chain { label="Blockchain rails"; labeljust="l"; color="#15803d"; fontcolor="#15803d"; style="rounded"; xrp [label="Ripple ODL\n(XRP bridge)", fillcolor="#dcfce7", color="#15803d", fontcolor="#15803d"]; xlm [label="Stellar\n(XLM / anchors)", fillcolor="#dcfce7", color="#15803d", fontcolor="#15803d"]; usdc [label="USDC\n(Circle CCTP)", fillcolor="#dcfce7", color="#15803d", fontcolor="#15803d"]; } // CBDC rail: wholesale + retail pilots subgraph cluster_cbdc { label="CBDC rails (wholesale + retail pilots)"; labeljust="l"; color="#6b21a8"; fontcolor="#6b21a8"; style="rounded"; mbridge [label="mBridge\n(BIS / CN, HK,\nTH, AE, SA)", fillcolor="#ede9fe", color="#6b21a8", fontcolor="#6b21a8"]; sand [label="Sand Dollar\n(Bahamas, 2020)", fillcolor="#ede9fe", color="#6b21a8", fontcolor="#6b21a8"]; enaira [label="eNaira\n(Nigeria, 2021)", fillcolor="#ede9fe", color="#6b21a8", fontcolor="#6b21a8"]; ecny [label="e-CNY\n(China retail pilot)", fillcolor="#ede9fe", color="#6b21a8", fontcolor="#6b21a8"]; deuro [label="Digital euro\n(ECB legislative)", fillcolor="#ede9fe", color="#6b21a8", fontcolor="#6b21a8"]; } // KYC/AML overlay applies to all rails subgraph cluster_compliance { label="Compliance overlay"; labeljust="l"; color="#b91c1c"; fontcolor="#b91c1c"; style="rounded"; kyc [label="KYC / AML\nOFAC, EU, UN\nsanctions screen", fillcolor="#fee2e2", color="#b91c1c", fontcolor="#b91c1c"]; travel [label="FATF travel rule\n(Recommendation 16)", fillcolor="#fee2e2", color="#b91c1c", fontcolor="#b91c1c"]; kyc -> travel [style=dashed, color="#b91c1c"]; } // Destination bankB [label="Bank B\n(destination)\nfiat: local", fillcolor="#dbeafe", color="#1d4ed8", fontcolor="#1d4ed8"]; // Bank A fans out to each rail bankA -> swift_msg [label="instruction", fontsize=9, color="#a16207"]; bankA -> xrp [label="on-ramp", fontsize=9, color="#15803d"]; bankA -> xlm [label="on-ramp", fontsize=9, color="#15803d"]; bankA -> usdc [label="on-ramp", fontsize=9, color="#15803d"]; bankA -> mbridge [label="wholesale", fontsize=9, color="#6b21a8"]; bankA -> sand [label="retail", fontsize=9, color="#6b21a8"]; // Each rail converges on Bank B nostro -> bankB [label="credit", fontsize=9, color="#a16207"]; xrp -> bankB [label="off-ramp", fontsize=9, color="#15803d"]; xlm -> bankB [label="off-ramp", fontsize=9, color="#15803d"]; usdc -> bankB [label="off-ramp", fontsize=9, color="#15803d"]; mbridge -> bankB [label="atomic PvP", fontsize=9, color="#6b21a8"]; sand -> bankB [label="payout", fontsize=9, color="#6b21a8"]; enaira -> bankB [style=dotted, color="#6b21a8"]; ecny -> bankB [style=dotted, color="#6b21a8"]; deuro -> bankB [style=dotted, color="#6b21a8"]; // Compliance overlay touches every rail (dashed, grey) kyc -> swift_msg [style=dashed, color="#b91c1c", arrowhead=none]; kyc -> xrp [style=dashed, color="#b91c1c", arrowhead=none]; kyc -> usdc [style=dashed, color="#b91c1c", arrowhead=none]; kyc -> mbridge [style=dashed, color="#b91c1c", arrowhead=none]; travel -> bankB [style=dashed, color="#b91c1c", arrowhead=none]; }

The three clusters compete on different axes. SWIFT GPI optimises for reach (11,000+ institutions, 200+ countries) and reuses bank balance sheets as nostro float. Blockchain rails optimise for settlement finality and the ability to bridge thin currency pairs without a pre-funded nostro on each side. CBDC rails optimise for central-bank control over money supply and instant gross settlement, with PvP (payment-versus-payment) atomicity demonstrated by mBridge.

4.4. Regulatory Considerations

Cross-border blockchain payments face complex regulatory requirements:

- Money transmission licenses in each jurisdiction

- Sanctions screening (OFAC, EU, UN lists)

- Anti-money laundering (AML) requirements

- Travel rule compliance (FATF Recommendation 16)

- Data localization requirements in some jurisdictions

5. References

- SWIFT: https://www.swift.com/

- Ripple: https://ripple.com/

- Circle (USDC): https://www.circle.com/

- BIS Innovation Hub: https://www.bis.org/about/bisih/

- FATF Travel Rule: https://www.fatf-gafi.org/

- World Bank Remittance Prices: https://remittanceprices.worldbank.org/

6. Notes

- The 2016 timeframe of this research predates many current stablecoin and CBDC developments, but the fundamental analysis of SWIFT limitations and blockchain potential remains relevant.

- Regulatory clarity has improved significantly since 2016, with frameworks like MiCA in Europe providing clearer guidelines.

- The "blockchain border bank" concept anticipated many developments now being implemented by both crypto-native and traditional financial institutions.

7. Related notes

- Blockchain identity and lending – companion 2016 note on the on-chain credit side of the same architecture.

- Agent token exchange – bot-native rails (x402, agentic micropayments) extend the cross-border settlement question to non-human counterparties.

- Software design – the layered-rails framing in this note maps to the bounded-context vocabulary used there.

8. Postscript (2026)

The 2016 framing held up better than expected on the structural side and worse on the timing. Ripple's On-Demand Liquidity (ODL) gained early traction with Tier-2 corridors but most large banks dropped active ODL pilots between 2022 and 2023; SWIFT GPI plus the ISO 20022 migration (deadline November 2025 for cross-border MX co-existence) absorbed most of the speed and traceability complaints that motivated the original note. CBDC pilots fragmented along policy lines: the Bahamas Sand Dollar launched October 2020, eNaira launched October 2021, the e-CNY remained a domestic retail pilot through 2025, and BIS Project mBridge reached minimum viable product in June 2024 before the BIS exited the project that October – leaving the participating central banks (PBOC, HKMA, BOT, CBUAE, SAMA) to continue independently. On the rails the original note underweighted: instant gross settlement systems (FedNow launched July 2023, SEPA Instant became mandatory 9 October 2025) and stablecoin corridors (Circle CCTP shipped 2023) ate the "fast cross-border" niche without requiring a permissioned blockchain at all. The agentic-finance overlay – x402 micropayments (April 2026) and bot-initiated transfers – is the new question that the original 2016 framing did not anticipate.